Chip giant Intel Corporation (INTC) is set to report its first-quarter results for fiscal 2026 on April 23 after the market closes. Ahead of that, analysts expect the company to report a loss per share of $0.11 (on a diluted basis). Intel has been recovering from its market share loss due to stiff competition from major semiconductor companies, most notably from Advanced Micro Devices (AMD).

Now, a lot of Intel’s hopes are riding on AI-driven data-center CPU demand and the ramp of the 18A process, with Q1 earnings as a possible near-term catalyst. Against this backdrop, Stifel analyst Ruben Roy raised Intel’s price target from $42 to $65, but kept a “Hold” rating on the stock. This indicates that the analyst is confident in Intel’s recovery but is not ready to call it a “Buy” unless the company actually executes on that conviction.

Intel has started this year by forging significant partnerships. The company deepened its partnership with Alphabet's (GOOG) (GOOGL) Google to advance the next generation of AI and cloud infrastructure, while it was added to Elon Musk’s Terafab AI chip complex project alongside SpaceX, Tesla (TSLA), and xAI.

We take a deeper look at Intel at this juncture…

About Intel Stock

Headquartered in Santa Clara, California, Intel designs and manufactures semiconductors, including central processing units and related components for business and consumer markets. The company operates through key segments such as client computing, data center and AI, network and edge, and Intel Foundry Services, driving innovation from Silicon Valley to its global facilities.

In the AI race, Intel accelerates development across edge, cloud, and PCs with tools like NPUs and Gaudi accelerators, aiming to bring AI everywhere securely. Intel has a market capitalization of $331 billion.

The company faces strong demand for AI PCs and server CPUs, fueled by advances in agentic AI that have boosted the client computing and data center segments. Foundry progress, plus geopolitical shifts favoring U.S. manufacturing, have rebuilt investor confidence.

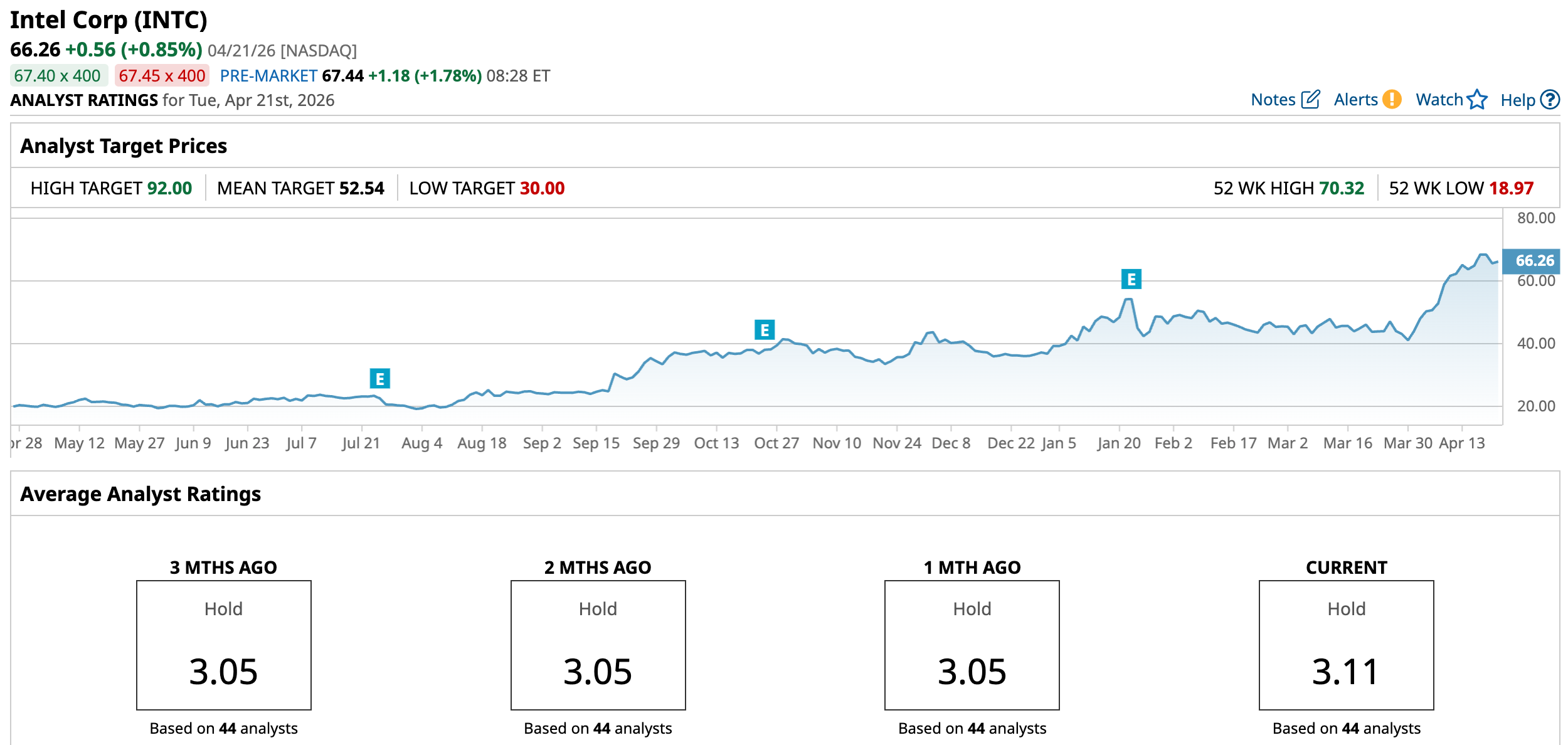

Over the past 52 weeks, Intel’s stock has gained 251.7%, while it has been up 79.57% year-to-date (YTD). It reached a 52-week high of $70.33 on April 17, and is down only 5.8% from that level.

On a forward-adjusted basis, Intel’s stock is trading at a price-to-sales ratio of 6.12 times, which is significantly higher than the industry average of 3.19 times.

Intel’s Q4 & FY25 Earnings

For the fourth quarter of fiscal 2025, Intel reported revenue of $13.67 billion, down 4% year-over-year (YOY), as the company experienced industry-wide supply shortages. However, the figure also exceeded the $13.37 billion that Wall Street analysts had expected. Its non-GAAP gross margin declined from 42.1% in Q4 2024 to 37.9% in Q4 2025. On the other hand, Intel’s non-GAAP EPS increased 15% YOY to $0.15, surpassing the $0.08 that analysts had expected.

For the full year, Intel’s top line remained roughly flat YOY, coming at $52.85 billion. The company also reported non-GAAP EPS of $0.42 for the year. Now, Intel is looking forward to the scaling of the Intel 18A products. The company expected its available supply to be at its lowest level in the first quarter of the current year and to improve from the second quarter.

Street analysts have robust expectations for Intel’s bottom line trajectory. For the current fiscal year, EPS is projected to surge 166.7% annually to $0.08, followed by a 562.5% increase to $0.53 in the next fiscal year.

Here’s What Analysts Think About Intel’s Stock

In addition to Stifel analysts’ view, Wall Street analysts have mostly had a mixed outlook on Intel’s stock. This month, KGI Securities analysts, led by Felix Pan, downgraded Intel from “Outperform” to “Neutral” and set a $71 price target. Analysts at the firm expect potential challenges due to current market dynamics and competitive pressure.

Bernstein analysts maintained a “Market Perform” rating on Intel’s stock, but almost doubled the price target from $36 to $60, which indicates that the firm is optimistic about the company’s turnaround due to its data center demand and robust foundry relationship with notable names like Google, Tesla, and xAI.

On the other hand, analysts at Benchmark maintained a “Buy” rating on Intel, raising the price target from $57 to $76, noting that the company’s recent announcements, including notable partnerships, could signal fundamental improvement.

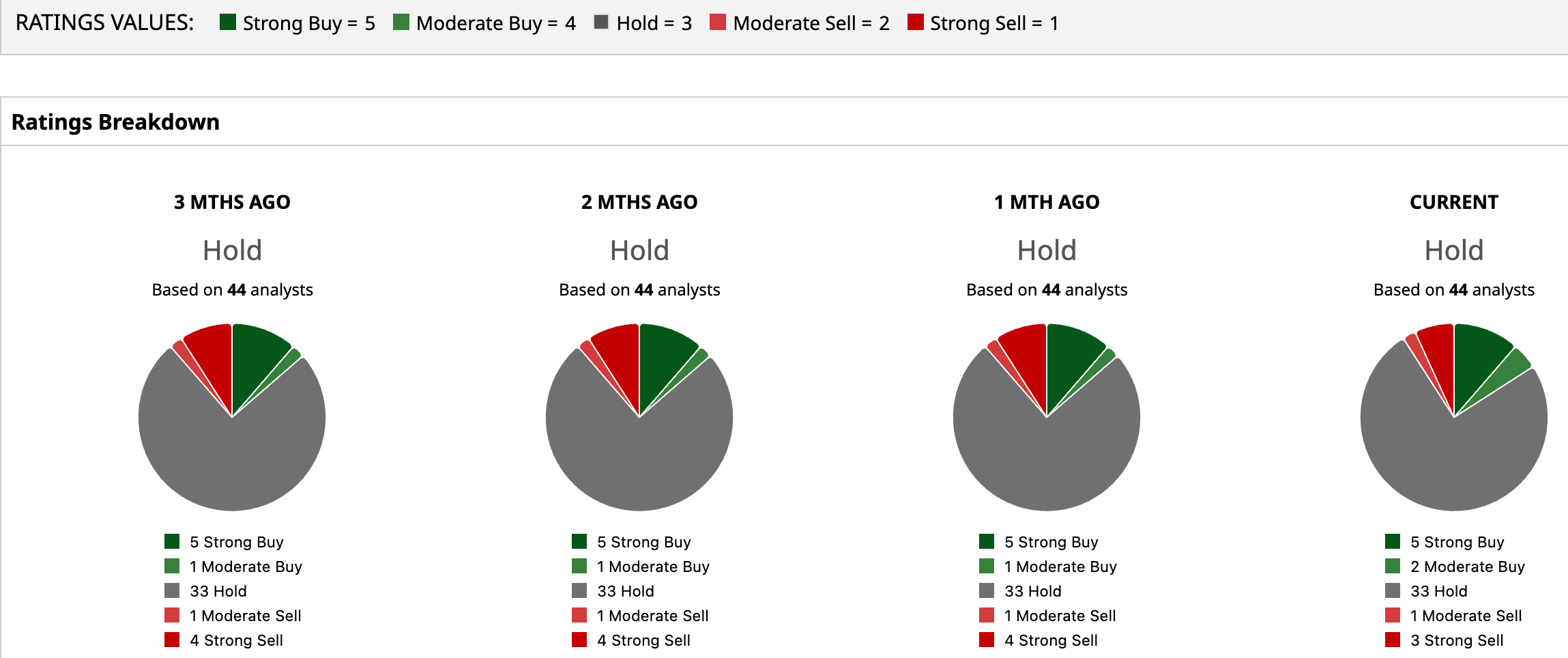

Wall Street analysts are taking a cautious stance on Intel’s stock, with a consensus “Hold” rating. Of the 44 analysts rating the stock, five analysts gave a “Strong Buy” rating, two analysts gave a “Moderate Buy” rating, while a majority of 33 analysts are playing it safe with a “Hold” rating, one analyst suggested “Moderate Sell,” and three analysts gave a “Strong Sell” rating. The consensus price target of $52.54 represents a 20.7% downside from current levels. However, the Street-high price target of $92 indicates a 38.9% upside from current levels.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?

- AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here?